The last 15 months have seen an incredible rotation of risk and returns and many of the names that offered opportunities last year have done phenomenally well, either because the feared drop in revenues never occurred, or because

lease refer to our unchanged analysis here.

At E470m EV, the proposed transaction is certainly good news for HEMA, but would take place just below our base case. We admittedly bought into the name late, but we had been

The agreement of the SSNs to what is essentially their own plan was only to be expected. The more interesting news yesterday lies in the detail of

The Ramphastos and the Ad-Hoc group were not able to agree on terms, despite the gap between implicit valuations arguably not justifying the incremental headache that SSNs now have to deal with. Ramphastos are

Please refer to our existing analysis here.

Hema’s press release today contained no news that would change our mind with respect to the name, but the statement contained a few data points that are worth mentioning:

Recent press articles have not been well managed. What they mean for the SSNs and SUNs.

- Ramphastos have not so elegantly chosen to

Below is an account of each of the names we follow and have begun work on in the context of Covid19 and Oil prices. Several names stand out as having become either uninvestible or outright attractive - already now.

Please find our updated analysis here.

We have contacted a Dutch retail specialist to confirm the touted

Hema had a few comments today that stood out to us:

1) The new distribution centre will be taken over in February. But it seems that

Also announced today was the final agreement with Jumbo. The agreement is very positive, if lacking in some key detail.

Main points:

1) Sale to Jumbo of 17 HEMA City stores in NL and Belgium over the next 3 years. Hema plans to replace

Hema results came in not far from expectation.

Deviations from model for Q3:

Sales: + E7m. LfL consumer sales of

Following an interview given by To van Veen, CFO of Jumbo supermarkets in a Dutch Dagblad, the market is speculating just how many stores Hema would be selling to Jumbo.

The deal:

- Little is known at this stage, other than that

Following last week’s restated segment earnings and some additional information on HEMA from a well informed source,

We have taken a position in the HEMA SSNs at 75c/E for 4% of NAV. Please find our updated in-depth analysis here.

LfLs continue to turnaround - even if they continue to

Hema with disappointing numbers this morning:

LfLs were positive in general. So far so good. Sales growth was primarily driven by hard goods.

The company refers to

On Friday HEMA announced a new partnership with Franprix (Casino) under which HEMA will be wholesaler to Franprix, supplying the French retailer with its range of non-food products. Financial details of

A stroll down the high streets of west London alone confirms the dire state of British retail. Shop fronts remain boarded up for years now, clearly unable to find a tennant in a market with static supply and ever decreasing demand

Please find our in-depth analysis and model of HEMA here.

Macro factors are not headed in the right direction for the company and its cost saving efforts are falling somewhat

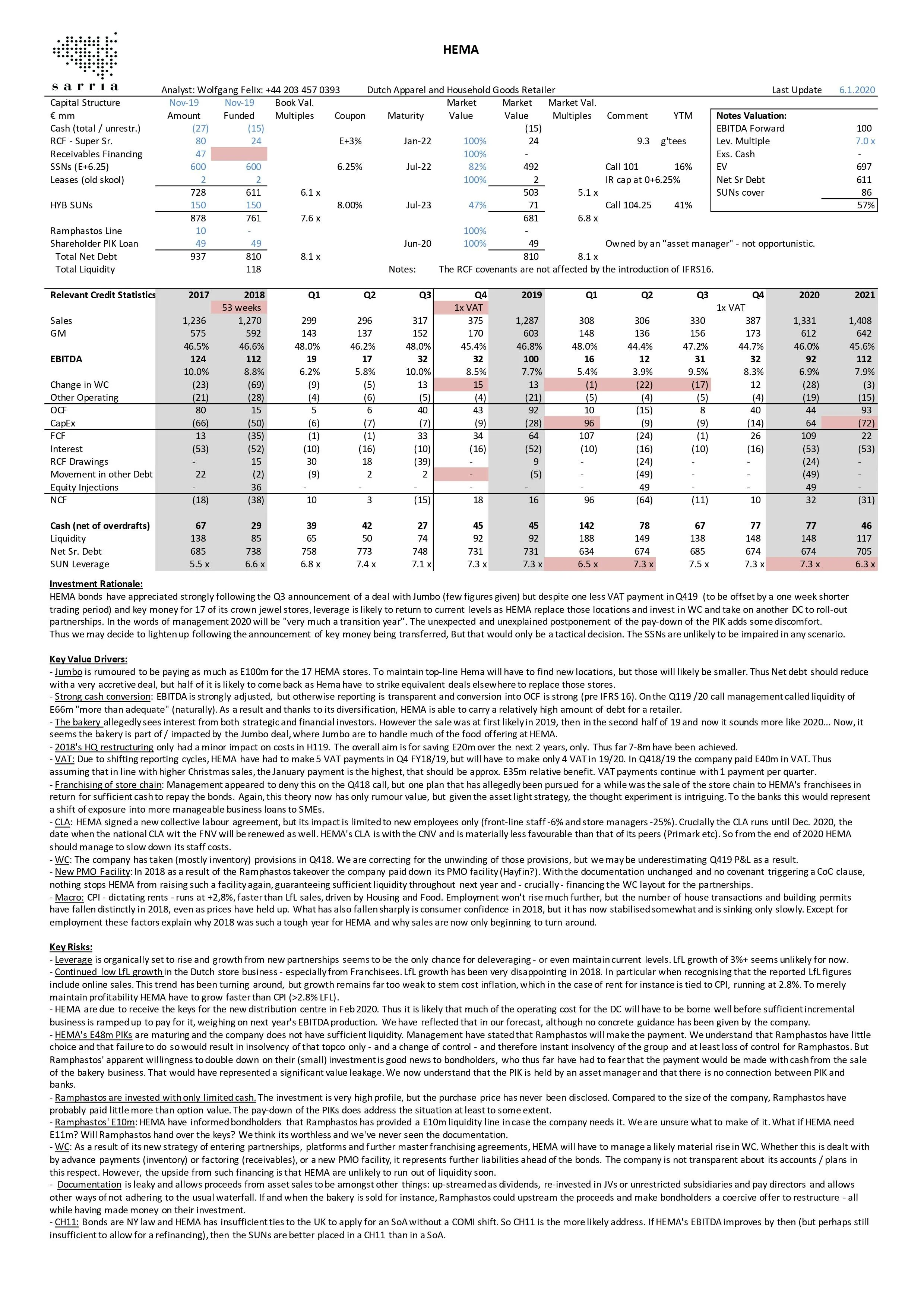

Please find our initiation on HEMA here.

HEMA is a case of a number of fundamental trends garnished with numerous transactional and

We are wondering if these appointed individuals would join that board (not turnaround professionals) without the confidence that Ramphastos are ready to significantly