UK Financial Restructuring Landscape in 2021 A Lookback in Bewilderment

December 2021

By Stephen Phillips, Temple Bright

Stephen Phillips | Partner

T. +44 (0) 20 7139 8233

M. +44 (0) 7811 113 895

Introduction

We face a rather uncertain end to the year. Just as we thought COVID was going to fade into the background of the long list of winter respiratory illnesses a new variant of concern arrives to blow up our assumptions – to paraphrase Al Pacino in the Godfather ‘Just when we thought we were out they pull us back in’.

The end of the year is a good time for reflection, and I address below the economic impact of the past two years of the pandemic and the key legislative changes and cases relevant to corporate restructuring and insolvency. I will no doubt miss aspects given the vast scale of changes resulting from the pandemic for which I apologise in advance - what follows is my own (perhaps idiosyncratic) view of key developments in the UK.

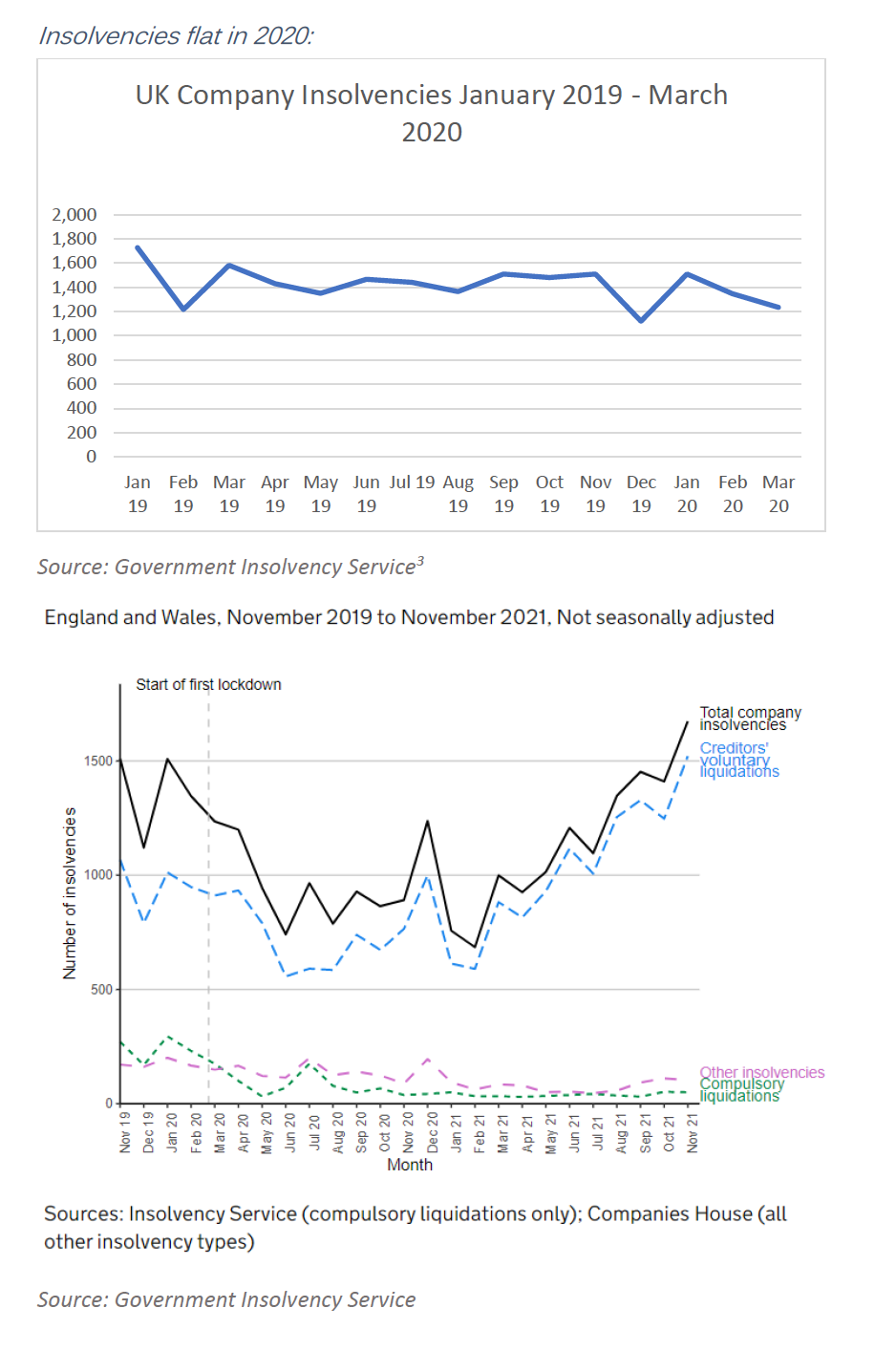

Restructuring and Insolvency Activity 2020/21

The advent of the New Year is accordingly less optimistic than was the case at the end of November, particularly for the hospitality and leisure sector. At the time of writing the FTSE 100 index is sliding back towards 7000 to reflect market gloom1. The Bank of England’s base rate increased from an all-time low of 0.1% to 0.25% to reflect the Bank’s concern on inflation which increased to 5.1 % in November 2021. Concerns regarding the new omicron variant / UK government measures taken in response have severely reduced Christmas revenue for hospitality even if it turns out that omicron is less problematic than we first thought. However, as we enter a state of soft-lockdown, as firms institute work from home policies, it is well to remember that industry has been here before and is likely to show a resilience and bounce-back ability compared to the sudden stop inflicted by the first lockdown. Damage is more likely to be concentrated in the hospitality and leisure sector albeit with knock on effects into other sectors.

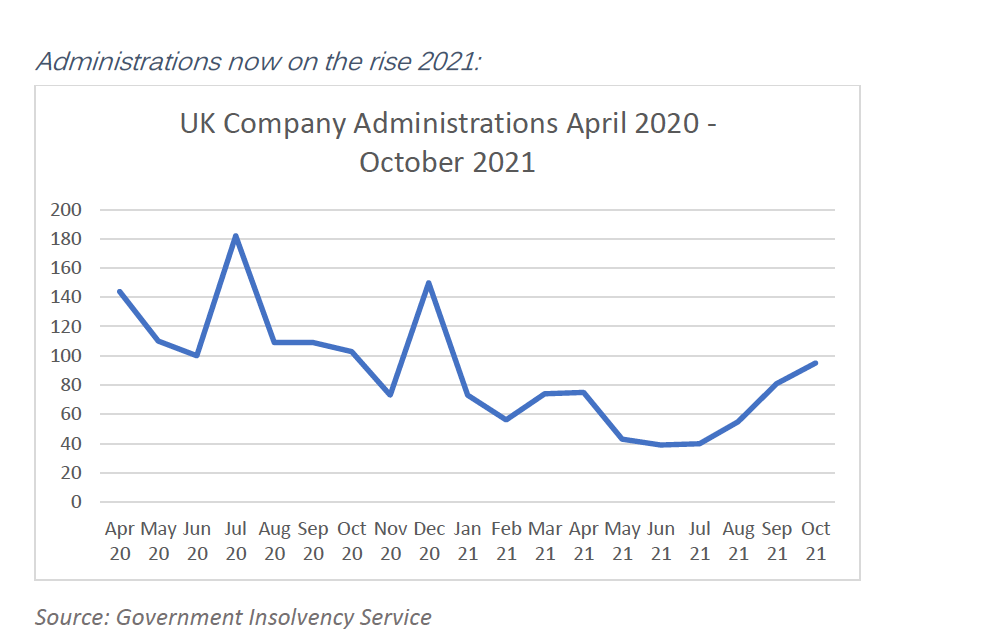

Real GDP contacted by a massive 9.9% in 2020 – and you had to look back to the Great Frost of 1709 to see a recession of such magnitude. Yet with massive government intervention (£0.3 trillion according to PwC)2, soft loans, generous furlough schemes, prohibitions on winding ups, measures to prevent evictions of commercial tenants, the UK experienced a decline in insolvencies and a significant decline in the number of companies in administration. Insolvencies are now, however, on the rise (as are administrations – one of the UK’s rescue tools). The November 2021 statistics were the first since the start of the coronavirus (COVID-19) pandemic to show the monthly numbers of registered company insolvencies were higher than pre-pandemic levels. We also note in the chart below that administrations are now on the rise.

1 Curious to think that the FTSE 100 index reached over 6900 in December 1999, and now hovers just over 7000. The significant increases in stock market values is largely a US phenomenon.

2 https://www.pwc.co.uk/business-restructuring/pdf/global-restructuring-trends-2021.pdf

3 Commentary - Monthly Insolvency Statistics October 2021

The Zombies Live On

Massive government intervention might be seen as a buy now pay later strategy, but the outturn has been a low unemployment rate and the avoidance of social dislocation. Zombie companies live to fight another day acting as a drag on long term productivity, but we avoided severe short-term economic pain. The decline in insolvency activity from normal levels has been remarkable given the circumstances. Ultra-low rates seemed to have lengthened the business cycle and made defaults very scarce – there has been little creative destruction.

There is a price to pay as the Bank of England’s paper ‘The Real Effects of Zombie Lending in Europe’ puts it:

‘Taken together… results suggest that forbearance lending practices contributed to the lower output experienced by the euro area following the onset of the European sovereign debt crisis.’4

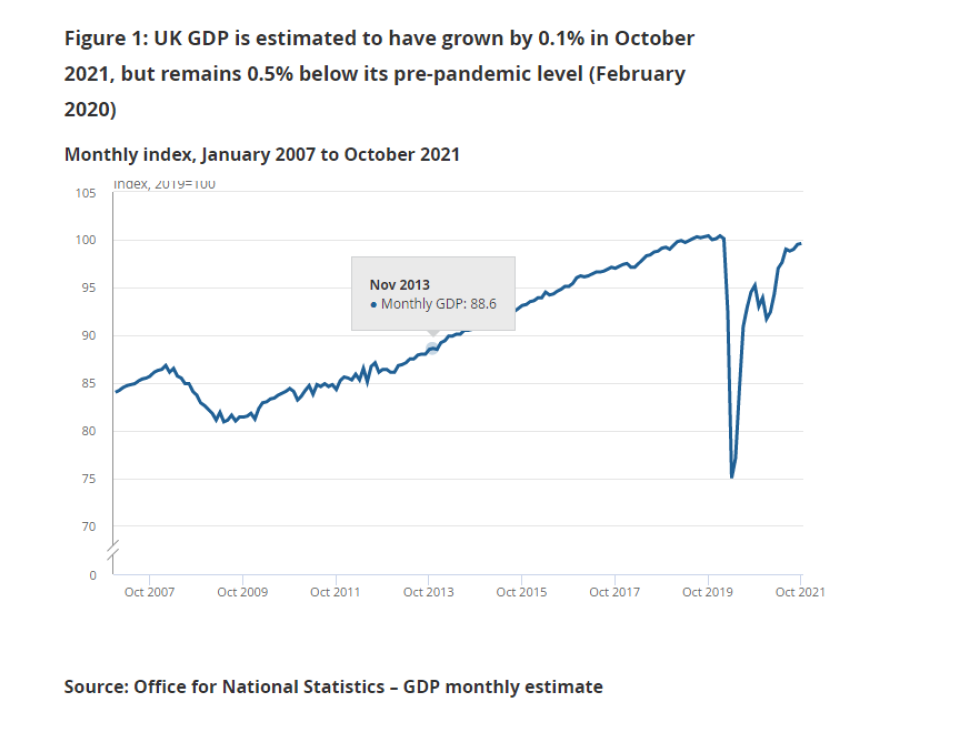

The exit from lockdown in July 2021 was accomplished with much grumbling but was elegantly done in my view with a very sharp rebound in activity as the UK became a beacon of liberality as far as COVID measures were concerned and this was reflecting in a strong set of growth statistics.5

4 Bank of England Staff Working Paper No. 783

5 GDP monthly estimate, UK - Office for National Statistics (ons.gov.uk)

Key Sector Stress

As the ONS chart above shows, Gross Domestic Product (GDP) is estimated to have grown by 0.1% in October 2021 representing a sharp slowdown, and the December COVID measures are likely to depress growth further. A number of sectors stand out in the Government Insolvency Statistics, construction, hospitality, retail and transport. A special mention should also be made of the 25 energy suppliers which collapsed in 2021 – it’s a fine example of what happens when governments impose energy price caps on smaller unsophisticated companies which do not have the wherewithal to hedge wholesale prices6. It has to be hoped the government gets the message that prices caps have severe downsides. My own experience has focused on two of these this year:

Construction

Looking back to 2020/21 some sectors have been under greater stress than others and my own practice this year has followed the key themes reflected in the wider economic picture. I have been assisting a director / shareholder whose bricklaying company, servicing the larger construction groups, which collapsed into insolvency having been caught by rising raw material prices, and increasing wages, turning a highly profitable business into an insolvent one as the company was unable to pass on the costs to its larger customers. I have also assisted a modular construction business undertake a sale through a ‘pre-packed’ insolvency to new investors. Whilst pre-packs are occurring with lower frequency than pre-pandemic times, they are still occurring and I address a key change to how they are implemented below.

Hospitality

The July 2021 reopening allowed the food and beverage service sector to grow by 8.9% in the three months to October 2021 according to the ONS. However, this sector was hit by three national lockdowns which eased on 19 July 20217 and the sector is likely to have a long-term hangover from two years of spotty (and sometimes non-existent) revenues. Many pubs and restaurants have built up significant rental and business rate arrears. Similar to construction, the sector has seen significant wage inflation and there have also been supply and logistical issues. Again, in the past 18 months I have been counselling a number of companies in this sector. The larger groups have been big enough to survive but smaller groups have either received further help from their owners or owners have or are about to leave the sector. The bounce back loan scheme was limited to £50,000 which was only likely to assist small pubs with short term liquidity problems. The wave of consolidation in the industry has only just begun. Small scale operators are going to become increasingly rare. All the above has been happening at the same time as the UK settles into its post BREXIT future and I turn below to some of the emerging issues as they touch upon restructuring.

6 For a list of insolvent companies - Which energy suppliers have gone bust? | energyscanner.com

BREXIT Themes

Recognition8

English law has often been the law of choice for many international contracts, including parties within the EU, a key example being loans documented under the Loan Market’s Association (‘LMA’) standard form. Prior to BREXIT a judgement in an English court was recognised in another EU member state without the need to re litigate the issue pursuant to the 2001 Brussels Regulation (44/2001)9. The British government recognising that English law is a great export earner for the UK judgments in civil and commercial matters between EU member states and Norway, Iceland and Switzerland sought to accede to the Lugano Convention10 which addresses recognition. The Convention clarifies which national courts have jurisdiction in cross-border civil and commercial disputes and ensures that judgments taken in such disputes can be enforced across borders.

Accession to Lugano?

To accede to the Convention, the UK's application will have to be approved by the EU, Denmark (which has an opt-out from certain EU justice conventions), Norway, Iceland and Switzerland. The UK’s accession is supported by Iceland, Norway and Switzerland but at the time of writing it appears the EU is opposed. It would seem likely that that the EU is hoping to reduce the influence of English law and use within the EU and capture more of the legal market within the EU.

Hague – the alternative?

Note that even if the UK is not permitted to accede to Lugano the UK is now a party to the Hague Convention on Choice of Court Agreements 2005 (‘Hague Convention)11in its own right. The Hague Convention includes rules on jurisdiction and enforcement of judgments across signatory states in circumstances where there is an exclusive jurisdiction agreement so this is likely to be a path for the UK to recognise EU judgements and vice versa.

The Hague Convention excludes a number of subject matters from its scope including ‘insolvency, composition and analogous matters.’ However, it might provide a basis for the recognition of schemes of arrangement, which are derived from the UK Companies Act 2006 and thus are sanctioned outside of insolvency proceedings. EU member states, Mexico and Singapore are bound by the Hague Convention and although it is not as favourable as the EU regime or the Lugano Convention, it provides a plausible substitute to the Lugano Treaty. The UK acceded in its own right on 1 January 2021. The Hague Convention only covers exclusive jurisdiction agreements whereas the main difference with Lugano is that the Lugano Convention applies to contractual relationships governed by non-exclusive and asymmetric (one-sided) jurisdiction clauses, as well as exclusive jurisdiction clauses. Counterparties who want to use English law will need to adjust their documents accordingly (as the LMA has done for its standard loan).

Insolvency and Scheme Recognition Issues – Post BREXIT Cases

Prior to BREXIT UK insolvency proceedings were automatically recognised in EU Member States via the European Insolvency Recast Regulation 2015 (‘Recast EIR’)12 (and vice versa). There were some legacy cases in 2021 where English courts were considering recognition under the Recast EIR. English courts are required to recognise EU insolvency proceedings if the applicable company had entered a proceeding prior to 31 December 2020. In Emerald Pasture13 the English court determined that even though the company was in a French sauvegarde proceeding that did not mean that the English law loan provisions relating to reporting covenants could be disregarded. Looking forward to proceedings stated after December 2020, however, any UK insolvency procedure will be determined under conflict of law rules of each relevant Member State’s jurisdiction, which is a far more idiosyncratic and less reliable method of obtaining recognition.

Scheme Recognition

Interestingly the question of whether a scheme of arrangement (which is not an insolvency measure) would be recognised in the EU was considered in DTEK’s scheme of arrangement.

In its scheme hearing DTEK14 produced expert evidence which opined that EU Member States would give effect to the scheme of the English law debt under the Rome I Regulation15 and Dutch private international law. The court in DTEK held that it would decline sanction for effectiveness reasons only if there was “no reasonable prospect of the scheme having substantial effect” i.e., that sanction would be in vain. The scheme was sanctioned but the true test will come in a case where recognition is considered in the court of a Member State of the EU and not in an English court. The English courts will recognise any foreign insolvency proceedings including companies from EU Member States under the Cross-Border Insolvency Regulations 2006 (CBIR)16, which implement the UNCITRAL Model Law on Cross-Border Insolvency in the UK, as occurred in the Greensill insolvency.17 Unfortunately the EU has not signed the UNCITRAL Model Law and this recognition is not available to

English companies/cases so there is significant asymmetry in the state of insolvency recognition between the EU and UK. In gategroup 18 the English court held that the new UK restructuring plan procedure under Part 26A Companies Act 2006 falls within the bankruptcy exclusion in the Lugano Convention. Whilst helpful for gategroup’s restructuring thus allowing the English court to have jurisdiction notwithstanding an exclusive jurisdiction clause in Swiss law governed bonds, the finding means a restructuring plan is likely to be considered not to fall within the purview of the Hague Convention (given how similar the Hague Convention is to Lugano). There is, accordingly, a lack of clarity as to how EU Member States will treat it. This may be one factor as to why schemes of arrangement may retain their utility given the example of DTEK above.

7 timeline-lockdown-social (instituteforgovernment.org.uk)

8 Recognition of Judgements Post-BREXIT by Stephen Phillips | LinkedIn

9 EUR-Lex - 32001R0044 - EN - EUR-Lex (europa.eu)

10 EUR-Lex - L:2007:339:TOC - EN - EUR-Lex (europa.eu)

11 HCCH | #37 - Full text

12 EUR-Lex - 32015R0848 - EN - EUR-Lex (europa.eu)

13 Emerald Pasture Designated Activity Company & Ors v Cassini SAS & Anor [2021] EWHC 2443 (Ch) (27 August 2021) (bailii.org)

14 Re DTEK Energy B.V. & anr [2021] EWHC 1456 (Ch) (convening); [2021] EWHC 1551 (Ch) (sanction)

15 EUR-Lex - 32008R0593 - EN - EUR-Lex (europa.eu)

16 The Cross-Border Insolvency Regulations 2006 (legislation.gov.uk) 17 Re Greensill Bank AG [2021] EWHC 966 (Ch).↩

The Corporate Insolvency and Governance Act 2020 (‘CIGA’)19

CIGA came into effect on 26 June 2020 and is the biggest change to the UK insolvency landscape since 1986.

Certain temporary COVID related provisions were included but most of the measures were designed for long term use with the key points being:

insolvent companies or companies that are likely to become insolvent can seek a 20 business day moratorium period which may be extended in practice by another 20 days;20

the directors stay in control (so this is similar to the so called /’debtor in possession’ concept in Chapter 11 in the US) but a monitor (an insolvency practitioner) will need to be appointed;

a new restructuring procedure has been introduced (which can compromise secured and unsecured debt);

creditors will vote on a restructuring plan in separate classes but a plan will be approved if a judge is satisfied that a dissenting class would be no worse off than the most likely alternative and that consent has been received from a creditor class representing 75% of those who have a genuine economic interest;

certain contractual provisions which engage on insolvency are prohibited.

The Restructuring Plan Cases

Virgin Atlantic and Pizza Express were the first two companies to test the procedures and the plans were successful without being challenged. There were a couple of challenges to plans which are worth highlighting one of which succeeded – DeepOcean2122 – and one failed, Hurricane23. The two cases shed some light on the willingness or otherwise of the courts to apply the new procedures of cross-class cram down as both featured dissenting classes – in practice the ability of a dissenting creditor class to be voted down in certain circumstances.

Two statutory conditions must be satisfied for a restructuring plan to be sanctioned:

Test A: the court is satisfied that no member of a dissenting class would be any worse off under the terms of the plan than they would be in the ‘relevant alternative’ to the plan (i.e. whatever the court considers would be most likely to occur if the plan were not confirmed); and

Test B: the plan has been approved by a stakeholder class who would receive a payment, or have a genuine economic interest in the company, in the event of the ‘relevant alternative.’

DeepOcean provided the ‘all other creditors’ class with a return of 4% above returns forecasted in the ‘relevant alternative’, which was an insolvency. Accordingly DeepOcean easily met the ‘no worse test’.

Even if the above tests were met the court still has a discretion to reject the plan on ‘just and equitable’ grounds. Unlike a scheme where creditors voting in the scheme must be treated equally a restructuring plan does allow for differential treatment of creditors and the court held that ‘the court will be concerned to ascertain whether there has been a fair distribution of the benefits of the restructuring (what some commentators have called the ‘restructuring surplus’) between those classes who have agreed the restructuring plan and those who have not’.

In Hurricane the court held that the company has not presented the relevant alternative correctly on the basis that the court did not believe a liquidation would immediately follow (which is what the company presented) and so it could not sanction as it failed Test A as articulated above. However, the judge explained that even if the relevant tests in A and B were met it would have not sanctioned the scheme regardless. In essence the company was still trading profitably and whilst a shortfall was forecast in the future it would not be equitable to immediately remove all the shareholders’ equity when the longer-term picture was not clear.

No doubt the cross-class cram down debate has only just begun.

18 Re gategroup Guarantee Limited [2021] EWHC 304 (Ch)

19 Corporate Insolvency and Governance Act 2020 (legislation.gov.uk)

20 The Insolvency (England and Wales) (No.2) (Amendment) Rules 2021 (legislation.gov.uk)

21 Re DeepOcean I UK Ltd & Ors [2021] EWHC 138 (Ch) (‘sanction judgment’)

22 I recommend an excellent review of the case by Kate Stephenson, and Zoe Stembridge in international-corporate-rescueenglish-courts-first.ashx (kirkland.com). The explanatory note to CIGA are helpful too Corporate Insolvency And Governance Act 2020 (legislation.gov.uk)

23 Hurricane Energy PLC, Re [2021] EWHC 1759 (Ch) (28 June 2021) (bailii.org)

End to Many Temporary Reliefs 24

For much of the pandemic winding up petitions have been prohibited save where a petitioner was able to prove that a company’s non-payment arose pre-pandemic. From 1 October 2021 until 31 March 2022, a creditor can only present a winding-up petition on the ground that the company is unable to pay its debts if each of the following conditions is satisfied:

the debt due by the company to the creditor is (i) liquidated (i.e., for a specific amount), (ii) has fallen due and (iii) is not an “excluded debt”, which is defined as rent under a business tenancy which is unpaid by reason of a financial effect of coronavirus;

the creditor has delivered written notice seeking the company’s proposals for the payment of the debt;

after 21 days, the company has not made a proposal for payment that is to the creditor’s satisfaction; and

the amount owed is at least £10,000.

24 End of temporary insolvency measures - GOV.UK (www.gov.uk)

Commercial Tenant Evictions Still Not Possible

Section 82 of the Coronavirus Act 2020 currently prevents landlords of commercial properties from being able to evict tenants for the non-payment of rent. This prohibition will continue until 25 March 2022. The government has announced it will legislate to ringfence rent debt accrued during the pandemic by businesses affected by enforced closures and set out a process of binding arbitration to be undertaken between landlords and tenants. As soon as legislation is passed, the commercial tenant protection measures will only apply to ringfenced arrears.

New Regulation for Pre-Packs

The Administration (Restrictions on Disposal etc. to Connected Persons) Regulations 2021 (the Regulations) came into force on 30 April 2021.

A pre-pack sale is a sale of the assets and business of an insolvent company negotiated prior to a company entering administration. The sale is carried out by the administrators almost immediately after their appointment. I view pre-packs favourably because they tend to minimise the loss of value to creditors and reduce the damage to relationships with employees, customers and suppliers that may result from a long administration. They are brutal but quick and have little court supervision relying on the professional integrity of the administrator who must be an insolvency practitioner. They were, however criticised by some and the government has attempted to address concerns with changes to legislation.

The Regulations:

commenced on 30 April 2021 and applied to a situation where the Administrator seeks to dispose of all or a substantial part of the company’s assets to:

○ a “connected person;” and

○ within eight weeks of the commencement of the Administration,

and either:

the Administrator must obtain the approval of the creditors before the sale can complete; or

the buyer must obtain a written “qualifying report” from an Evaluator on whether the grounds and consideration for the disposal are reasonable.

My experience is that seeking creditor approval for a pre-pack seems unlikely. Often a pre-pack occurs in difficult circumstances where not all creditors are particularly supportive of a company and/or where an unexpected liquidity shortfall has occurred, and wages are shortly to be paid. Accordingly in the recent pre-pack I advised on an Evaluator’s report was obtained and I expect that to be the procedure going forward for most of the cases - for pre-packs, time is of the essence.

Directors’ Conduct

New legislation, Rating (Coronavirus) and Directors Disqualification (Dissolved Companies) Act 2021 ('the Act') does away with a previous burdensome requirement that companies needed to be restored to the Companies House Register if the Insolvency Service wished to investigate the conduct of the directors of a company which had been dissolved. The Company Directors Disqualification Act 1986 has been amended to allow investigations of, and disqualification proceedings to be brought against, such directors. Most of the provisions of the Act relating to directors’ disqualification will come into force two months after 15 December 2021.

Insolvency Services

On 21st December 2021 the UK Government launched new proposals to reform and simplify regulation of the insolvency sector. Key changes set out in the consultation include:

• establishing a single independent regulator to sit within the Insolvency Service, replacing the current four Recognised Professional Bodies

• extending regulation to firms that offer insolvency services, as the current regime only covers individual Insolvency Practitioners (‘IPs’)

• create a public register of all individuals and firms that offer insolvency services

• create a system of compensation and redress

The UK tends to be ‘light touch’ when it comes to the involvement of the court during liquidations and administrations which for the most part means administrators and liquidators can get on with the job to drive for the best commercial result for creditors. However, given the power given to IPs I welcome the addition of a possible remedy for poor behaviour given that removing an IP on a case is extremely difficult and costly. It’s likely that outwardly this will make little change to the practice of IPs.

Future

Rising interest rates, rising prices, slowing growth, pressure on hospitality and travel in particular points in one direction – a growth in insolvencies and restructuring activity. The measures taken to date have ‘squashed the insolvency sombrero’ but in 2022 work needs to begin in earnest to restructure the economy. The ‘zombie’ problem has gone on far too long and is a severe drag on the economy. The largescale commercial rent arrears will need to be addressed. We await the details of the binding arbitration process between landlords and tenants discussed above but expect most situations to be resolved informally.

There are plenty of excellent restructuring tools available with schemes of arrangement and the new restructuring plan available for the larger complex cases, with less costly and easier to implement company voluntary arrangements to address unsecured debt. Where companies face an immediate crisis pre-pack administrations remain available albeit with the tweak in implementation mentioned above, and for terminal cases winding up petitions have been available since 30 September 2021. Directors retain the option to liquidate. Long administrations are rare, but they still can be useful in certain appropriate cases.

Expect an acceleration of corporate restructuring, insolvency, and M&A consolidations in 2022. There is according to PwC an enormous well of dry power in the private markets to utilise. Much of the distressed debt funds have struggled for opportunities in the past few years.

A client in the retail sector recently told me that he had seen ten years of innovation in a year. There are some businesses very well positioned for growth and further innovation. A period of economic pressure and social change is often a driver for opportunities. For example, in the oil sector it is obvious that we are seeing increasing pressures on the oil majors to stop producing oil for environmental reasons and an indirect pressure on traditional funders of oil to stop funding. Oil will remain necessary, however as we transition to renewables and new nuclear. As traditional reserve base lenders and the capital markets withdraw from the market this will place tremendous strain on oil companies as they are starved of capital. This provides a tremendous opportunity for alternative credit providers and family offices to step in and provide funding to fund the transition and the decommissioning phase.

It’s an obvious point to make but all the financial restructuring over the next few years will inevitably be accompanied by operational restructuring to allow businesses not just to survive but to thrive. Many of us in the industry look forward to playing our part, however small.

Stephen Phillips, December 2021

……………………………………………………………………

• This presentation is given by Stephen Phillips for Temple Bright LLP (both of whom are together referred to hereafter as “we”This presentation is given by Stephen Phillips for Temple Bright LLP (both of whom are together referred to hereafter as “we”, , “u“us” and “our”). It is not intended to provide tax, legal or investment advice. You should seek independent tax, legal and/ors” and “our”). It is not intended to provide tax, legal or investment advice. You should seek independent tax, legal and/or investment advice before acting on information obtained from this presentation. We shall not be liable for any mistakes, errinvestment advice before acting on information obtained from this presentation. We shall not be liable for any mistakes, errors, ors, inaccuracies or omissions in, or incompleteness of, any information contained in this presentation, nor for any delay in updainaccuracies or omissions in, or incompleteness of, any information contained in this presentation, nor for any delay in updating ting or omission to update the information as we have not undertaken to do soor omission to update the information as we have not undertaken to do so

• We make no representations or warranties We make no representations or warranties regardingregarding the contents of and materials provided in this presentation and exclude all the contents of and materials provided in this presentation and exclude all representations, conditions and warranties, express or implied arising by operation of law or otherwise, to the frepresentations, conditions and warranties, express or implied arising by operation of law or otherwise, to the fullest extent ullest extent permitted by law. We shall not be liable under any circumstances for any trading, investment, or other losses which may be permitted by law. We shall not be liable under any circumstances for any trading, investment, or other losses which may be incurred as a result of use of or reliance on information in this presentation. All such liability is excluded to theincurred as a result of use of or reliance on information in this presentation. All such liability is excluded to the fullest extent fullest extent permitted by lawpermitted by law

• Any opinion expressed herein is a statement of our judgement at the date of presentation and is subject to change without Any opinion expressed herein is a statement of our judgement at the date of presentation and is subject to change without notiacenotiace

• Reproduction without prior written permission of Stephen Phillips of Temple Bright LLP is prohibitedReproduction without prior written permission of Stephen Phillips of Temple Bright LLP is prohibited