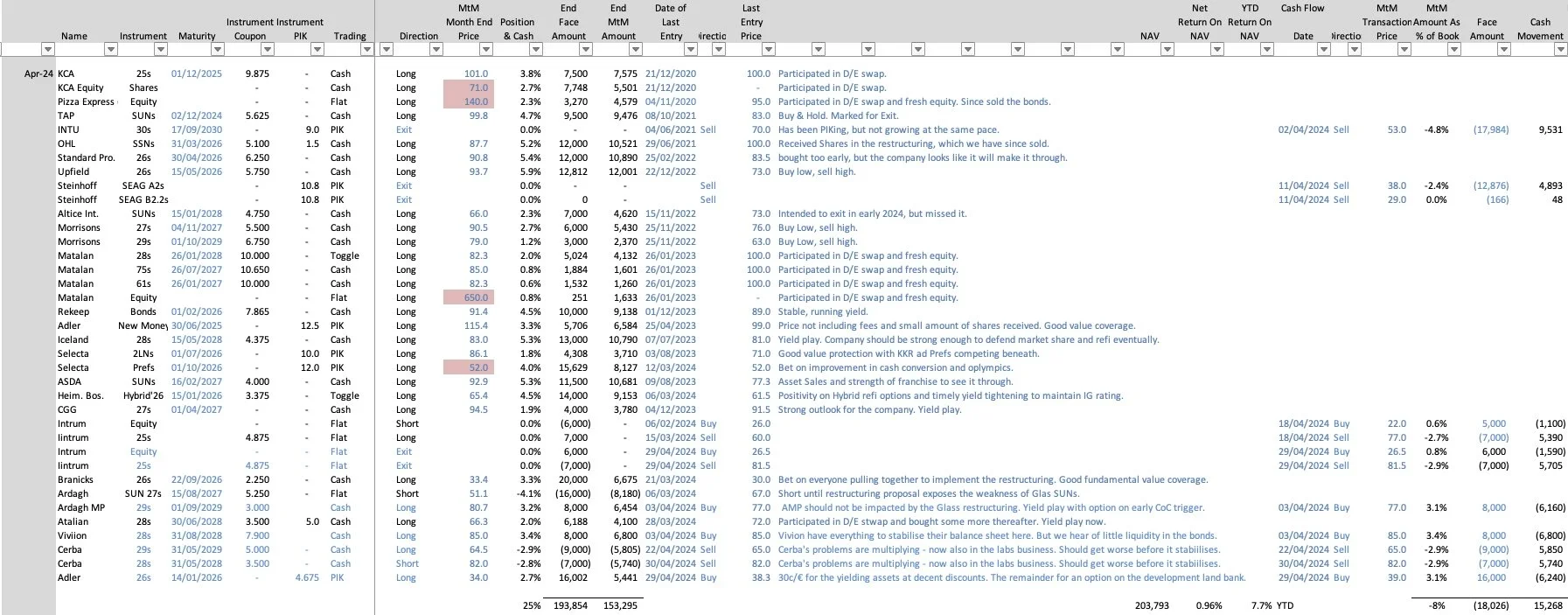

Sarria Nav - March 2024

SARRIA SHADOW BOOK

Contact the team: team@sarria.co.uk

RISK SUMMARIES

📕 icon indicates credits currently on our book, please see Track Record.

YIELD

-

AMS Osram: A yield play, and with a 10.25% cash coupon there is significant support for this yielding name. Convexity is limited at current prices, but yields are likely to tighten to 8%, implying 2pts of upside. In the next 6 months' trading levels will be determined by the degree of success of the exit from the Kulim factory, which should reduce leverage. Operationally, the turnaround is expected from H2, which will further support trading levels. Downside is unlikely from operational issues, but mainly on increased costs from exiting the Kulim facility which could see the bonds trade down to mid-90%.

The converts have the natural pull to par given their short maturity but the low coupon reduces the natural buyers of the paper, letting these bonds trade a little wide of the new higher coupon bonds.

-

Antolin: Upside:- The senior secured notes due 2026 are trading in the low 90s and have rallied in Q4 2023 and into 2024 in line with the credit markets and ahead of a gradual fundamental improvement in the company. As we expect a refinancing of the 2026 notes in the next fifteen to eighteen months – there is another ten points of upside (coupon and capital appreciation). If the growth in the company accelerates over the next fifteen months, we can expect a complete refinancing of the debt structure including the 2028 notes (which will include twenty-three points of upside from coupon and capital appreciation). However, we remain on the sideline until we see an acceleration of cash generation which would be supportive of the above.

Downside:- We feel the downside is ten to fifteen points on either of the notes (YTM of 15%) if EBITDA and cash generation does not improve materially. The company would look to its lenders to support a refinancing on terms which would be more advantageous than the bonds despite their pari-passu status.

-

AroundTown: With the unsecured bonds trading at 7-11% range and 5-8% range for AroundTown and GCP, we see limited upside/downside due to its asset coverage, no envisaged refinancing issues and no near-term event triggers. On the Hybrids, running yields are c. 15% at AroundTown, which is starting to become attractive. However, without a clear path to refinancing and the Company likely not to call upcoming hybrids at reset dates, the hybrid bonds are without a natural holding base.

-

ASDA: The SSNs yield 5.7% (97p/£), whilst the small SUNs yield 7.8% (91p/£); we prefer the additional pick-up offered by the SUNs. The SUNs' mature in Feb-27, but they are likely to be refinanced in Feb-25 in a refinancing of the capital structure, which equates to an 11% return. With two large shareholders beneath the SUNs and given their small size, we do not see this instrument at risk of an opportunistic restructuring without also significantly impairing the SSNs - should events deteriorate dramatically, that is. If inflation were to return to the recent highs, the downside would be 7 points (to a YTW 10.5%) ASDA is the 3rd largest supermarket in the UK, its market share is stabilising, and our analysis shows significant EBITDA improvement over the next 2-years. We have been conservative in our valuation analysis, but our DCF still has £1.6bn in equity value. The downside comes if food inflation rises significantly again and further price support is needed. In this scenario, ASDA has £9bn of freehold assets and could engage in sale and leaseback deals to generate liquidity.

-

Atalian: The Atalian Bond exchange was successful with over 90% consent, which meant the company was able to bind all holders to the deal. We value the package at 90c/€, and the market value is 81c/€. We expect trading at Atalian to improve in FY 2024, albeit slowly, with a significant recovery in 2026/2027. The next catalyst is the Q1 results, due in a month. The noise of the restructuring will have passed through, and we expect momentum to be behind the bonds. The upside is 9 points if the new bonds trade to c15%. The downside is 5 points if the 2028’s trade out to 28%. The new 3.5% 6/2028 bonds are currently trading at 67c/€ (YTW >15%). On a DCF basis, the price of the exchange bonds should be around 86c/€

-

CGG: We see potential upside for the € notes as the more robust operating environment flows through to the bottom line. A refinance in 2025/26 will also help pull the bonds towards par. The €7.75% are trading at 93.75 /EUR. The notes traded above par before the Ukraine conflict, the ratings of B3/B- will assist in opening up the CLO bid for new paper. The downside would be five points if the oil price were to fall below $80bbl for a protracted period. Oil price forecasts are for a price of €93bbl in 2024, and our analysis still points to continued capex boosts from new E&P as part of energy security plans which will benefit CGG.

-

Elior: Elior bonds trade at 88c/€ after a strong H2 performance. A covenant breach is now unlikely with the March 24 test loosened and our model showing compliance going forward. We expect the bonds to be refinanced in July 2025, on leverage of between 4.25x and 4.50x. The upside is 12 points + 3.75% in coupon for 18 months. However, the downside is material if there is a further resurgence in inflation and/or a significant recession in France. The bank facilities now mature at the same time as the bonds, which should keep management focused on getting the refinance done in good time.

-

Iceland: Upside: YTM of 8-9%. The new bonds are call constraint. There is only convexity in the 2028 low coupon bonds. We remain comfortable with the name and could envisage the bonds trading in a 7-8% YTM range, giving 5pts of upside on the longer-dated bonds.

Downside: Limited on an idiosyncratic risk basis. Possibility for the bonds to widen to 10% yields, but with no numbers until July and the Company comfortably guiding £170m+ EBITDA (post leases) we don’t see much risk. A wider grocery price war is possible but there are no major signs from the larger retailers that this is likely.

-

KCA Deutag: Upside: Around 95c/€, yield to maturity (worst) is 12% to Dec. 2025 with potential upside from an early call. Leverage is 1.2x pre-acquisition with new PIK and equity raise ongoing. Bond documents prevent significant increase of leverage at bond level (2.5x incurrence test), protects the downside on this bond. Other downside is in relation to their Russian business, which is 25% of their EBITDA.

KCA have the wrong capital structure, with bond maturity of December 25. Wage inflation is real concern, but KCA Deutag continues to gain contract extensions.

-

Maxeda: In the high 70s, the name yields a handsome 18% to maturity. However, this price also reflects the few drivers that will allow for such redemption on time. Maxeda will have to grow the business to support this level of debt and we see no idiosyncratic leavers. That makes it - on the upside - an unleveraged bet on Benelux consumer sentiment and other macro factors.

On the downside and even in the “nothing happens” scenario, the bonds will be unable to refinance. In that case the bonds look set to take control of the company in a second D/E swap. But the value in the equity will be limited and we doubt the new capital structure would trade close to current-bond-par after the event.

-

Morrisons: The GBP SSNs yield 8.3%, whilst the SSNs yield 12.7%. The yield differential between the SSNs and SUNs is compressing. We see another 5 points of upside in the SSNs in the next 12 months as rates fall (3 points) and spreads compress (2 points). We see 6 points of upside for the SUNs for the same reasons. The respective returns in the next 12 months are 11% and 14%. Morrisons has continued to direct cost-cutting to price support, so the margin improvement is taking longer than we initially expected. The sale of the petrol forecourt business will reduce leverage to <6.0x (ignoring the prefs, 7.6x with them). Morrisons will look to refinance the Parent Finco 2029 SUNs on November 27, along with the SSNs. The £1.9bn net proceeds of the Forecourt sale will be used to reduce debt, starting with the TLA. Bank debt is more expensive than Morrisons bonds, and we expect there will not be a bond tender.

-

Ocado bonds (SUNs and Converts) currently yield around 8%. The upside is 7 points of capital gains pa + 1.75% in coupon => 10% YTM The downside is around 15 points, the Retail JV with M&S covers the bonds c50% so at a price of 66 to 76 (depending on which bond), the downside risk is 15 points if we don’t see any improvement in the Retail business over the next 2-years. Growth in Ocado's Tech business is beginning to be visible, as Ocado begins to deliver CFCs to its supermarket partners. Tech is very much an equity story. The UK-based retail business is facing challenges with inflation and top-line headwinds as demand for online shopping normalises. We have been waiting for investors to become more focused on international growth over the traditional UK Retail business, but that hasn’t happened yet.

-

OHLA: We are long 6% NAV in the bonds and expect a 90bp return on NAV over the next six months. We will be selling our 1.8% position in the equity, which currently trades at 38c. The backlog is increasing more slowly and activity is likely to be flat in 2024, but the overall outlook for infrastructure spending is strong in both the US and EU. OHLA still hadn’t secured the release of €140m in cash held by the banks as collateral, but guarantee lines have been extended beyond 1 year. The downside is if the construction market deteriorates quickly and governments suspend infrastructure projects. This is mitigated by the post-Covid infrastructure investment funds (US/EU) that are still in place. The downside risk is up to 140bp of NAV, but we consider the upside far more likely.

-

Punch: Bonds offer 10% YTM in the most likely scenario. On a normalised LTM basis the company’s FCF only covered interest by £10m. But Punch have two years to re-build their margin, which has gotten hit by sharply rising raw material and wage cost as well as an egregious energy contract. PubCos are able to pass on their cost inflation, however, via steep price rises in beer. So we model EBITDA growth for the coming two years to approx. £90m, which should make a refinancing tight, but should - with a limited amount of fresh cash - allow at least for an amend and extend. On the downside, the bonds have little net debt ahead of them and are value protected by the real estate. We consider the Savills valuation excessive, but all things considered, the bonds would be the fulcrum under about any restructuring scenario. Safe for that, we see 80p/£ as the lower trading range from adverse news.

-

Rekeep: Overall, this name has no hard catalyst. Short-term we expect a small catalyst in the form of a larger than normal working capital inflow in Q4 to recover the recent 2-3pts drop in the bond price on reducing leverage. At 13% we see some 3-5pts of upside. Notwithstanding our generally positive view, we acknowledge that in the longer term, this credit is likely to trade sideways in a 10-13% range. This is due to only minor deleveraging, less than was expected at the time of the refinancing in 2021. We expect refinancing in FY25, which we think of as difficult but achievable.

Downside is limited. However, with only minor deleveraging expected, this bond could drift off to 15% yield (4-5pts downside).

-

Selecta: The SSNs and even the 2LNs look well value covered here and trade on a yield basis accordingly. We do not think that KKR are looking for an exit as soon as 2024 and so are paying no attention to the 20%+ YTC on the 2LNs for instance.

As regards the Prefs, their pricing reflects the uncertainty of whether these will be paid on time. Non-payment at maturity does not automatically constitute a default. Rather they can be converted into 100% of new common shares, where the KKR portion becomes non-voting. These instruments have therefore a weaker pull-to-par rationale than the bonds. Also, in a refinancing the sponsor may choose to subordinate/equitise their portion and thereby allow the SSN Prefs to be rolled into the new financing at what we think will be 5x LTM EBITDA by then.

-

The SSNs should be worth par in a straigth refinancing. Only a negative event or a strong market deterioration look capable of derailing that train. In that case, we still see an A&E possible in which the SSNs alone could extend to 2028 (2LN maturity) or both could extend longer.

The 2LNs are not currently covered in our opinion and still require either help from TDR or much improved results. That improvement looks like it will be forthcoming, but that will still take some time. TDR look unlikely to be losing this company now to the 2LNs. Their downside comes more from an aggressive/coercive A&E offer from Stonegate/TDR and that seems somewhat uncalled for now.

-

Upside:- The senior notes have rallied substantially into 2024 as the fundamental story of the Company continues to improve (organic growth, free cash flow generation and deleveraging). As we expect a refinancing of the notes in the next twelve months - there is another ten points of upside (coupon and capital appreciation). We remain constructive on the name given the defensive nature of the business, lower cost vs. substitutes of the product and good operational execution by management.

Downside:- We feel that downside is limited to five points to reach recent spreads of 11% again. The Company is in a defensive sector with free cash flow, price elasticity and positive organic growth which will continue into 2024.

-

Vivion: Vivion has sufficient levers to deal with the €183m August 2024 maturity. There is no rational scenario where the Dayan family lose over €1.5bn in net assets for the sake of an additional €100 - €125m. There is over €1bn in unencumbered assets in the UK hotel business and >€200m in the Ribbon assets net of the €230m M&G loan. There are no further public maturities until August 2028 allowing Vivion to benefit from decreasing cap rates driven by falling interest rates in € and £. The 2028 bonds yield 11.5% + 1.75% PIK. We see the bonds as covered by asset value and the next significant maturity will be the August 2028 notes. The downside is 20 points if there is a further significant rise in inflation. The next catalyst is at the end of April with the FY23 results publication. We expect a liquidity update but the impact on the longer-dated bonds will be small unless there is a revaluation well over 10% (our valuation is already 7% beneath that of the company.

-

VMEDO2: Catalysts for tightening for the SSNs are limited in the near term. The price rises have not led to a significant fall in subscribers, and a widening in bond spreads has not happened. The SUNs trade only about 100bp wide of the SSNs, so are not attractive either. Our analysis has EV covering the debt stack. As a place to park money, a yield of 9% for 5-year SSNs is not a bad return vs. bank deposits. Cable bonds have become such a staple investment for European investors we would not expect VMED to struggle to issue either bank or bond debt (a recent 5-year TL was upsized from £500m to £600m). VMED has £1.7bn of bank debt maturing in January 2027 with £675m of bonds in April 2027.

EVENT DRIVEN

-

Accentro : Accentro cannot make mandatory €40m in bond redemptions due in December 2023 and bondholders have approved that the payments be postponed. The bonds are trading at 38c/€ vs a recovery value closer to 30c/€. Only 20% - 30% of the assets are held under the double lux-co structure, which offers more creditor control of any enforcement process. The assets held under the German HoldCo would be sold by a local administrator with the proceeds eventually passed to creditors. The upside (15 points) would come from significant asset sales in 2024. Accentro will not sell at what they consider to be a discount. Nothing is changing here It’s an equity option primarily paid for by bondholders, and we will be back again next year.

-

Adler: The New Money and ARE bonds are safe. The ADJ bonds are value covered at approx. 30 c/€ from Brack and the yielding portfolios only. The few cents above that price are for the option that Consus could triple recoveries - in time. Adler cannot attract a reasonable bid for the land bank in this market and investors will have to wait for construction to resume in Germany. The country (thankfully) continues to suffer from a housing shortage, so this could be a lot sooner than in China for instance.

-

Altice International: The short-dated bonds (2025 maturities) are cash collateralised and offer near 10% for less than 1yr paper. The downside in theory is minimal but with the aggressive stance at Altice SFR, there is no confidence in the market that Altice International will be any different. The impact of SFR has caused the Senior bonds at Altice International to widen to 10% yields. This is 4 and 5yr paper and the downside risk centres on the Portuguese asset being divested leaving a 4-5.0x leveraged EM Company. The upside is partial or full repayment following sale of Portuguese and/or other assets.

At the sub-level, currently at 66% or 18% YTM, the upside is a pull to par following a successful divestment. The downside is similar to seniors if there is a large dividend without substantial debt repayment. The underlying business is strong and continues to deleverage.

-

SFR Altice France: We see limited upside in the Senior bonds in the foreseeable future. The bonds currently trade at 11-12% range for the medium term bond, with even in the most optimistic outlook, leverage would still be c.4.0x through the seniors where bonds would unlikely trade inside 10%. However, with the bonds trading in the low 70’s downside is limited due to likely high recovery value under any restructuring scenario, given the lack of debt ahead of the senior bonds.

The sub bonds are different. Yields, not that they matter, are in the low 30% level, but more importantly, the bonds are trading at distressed levels already at 40-50c. If it came to it, these bonds could be cut loose entirely under what would likely be a French restructuring scenario with the value line falling almost certainly inside the Seniors. Further complicating the recovery on the subs is the fact the Drahi/Next hold some of the sub bonds and may buy back more in the coming weeks and months. There is no liquidity concerns in the short term, but with a refinancing looming in late FY26/FY27 the sub bonds are highly vulnerable.

-

Ardagh: We see up to 20 points of downside for the Ardagh Group SUNs and a near wipe-out for the ARD Finance PIK toggles, triggered by the restructuring proposal will likely be made after the summer. The risk to the position is an unexpectedly generous offer to the SUNs which could see the bonds rally 10 points (in line with where they traded before the appointment of advisors).

The Ardagh Metal Packaging (AMPBEV) SUNs have recently widened on the back of the turmoil at Ardagh Group, but we see AMPBEV leverage falling in 2024 and 2024, and see 8 points of upside in the bonds in the next six months with the potential for 16 points if ARD disposes of its 75% stake in AMPBEV, triggering a Change of Control (we see this as unlikely in the near term). The downside for the AMPBEV SUNs is five points if the US recovery is slower than expected. There is no cross-default language between Ardagh Group and AMPBEV.

-

Atos: Without putting in fresh equity, we view Atos structure as uninvestable. The level of dilution expected from even the Company’s prospective case is significant, and our core view is that this is not even enough. The initial investment provides the opportunity to provide the fresh cash without investing more money, we see recovery in the single digits for Atos creditors.

Investors who are able to take part in the new money requirement will require to make 2x their fresh cash investment, but this is subject to negotiations and what level of debt write-off is achieved.

-

Boparan: Currently trading at around 67p/£, Boparan's bonds reflect concerns that the company will not be able to sell a deal to the high-yield market by November 2025. Our base case is that Boparan has managed profitability many times over to get refinances done. With underlying profitability improving and customers incentivised to avoid disruption, we are not willing to bet against another rabbit coming out of the hat. What gives us confidence is that Boparan has a very transparent cost structure. If the supermarkets wanted to push Boparan over the edge, they would gain nothing, but an administrator to deal with. Upside in a par refinance is 33 points of capital and 7.5 points in coupon => >60% in 12 months. The downside is at least 20 points, as the intertwining of the Boparan family in the business would pose a challenge to any restructuring.

-

Branicks: The company has now successfully rescheduled its 2024 maturities. The Bridge Loan maturity has been pushed to December 2024, and the Promissory Notes to June 2025. The SUNs trade at 34c/€, implying a significant probability of a non-consensual liquidation process where recovery would be zero. Our valuation of the SUNs is 65c/€. We consider the liquidation of Branicks to be an outlier, although we cannot rule it out. The secured bank facilities are comfortably asset-covered, but a liquidation would lead to losses. Instead, we expect Branicks to look to complete an amend and extend of the notes.

-

Upside:- The secured notes due 2029 are trading in the high 60s and have declined in 2024 due to the weak results and negative news flow around other large French restructurings. The senior secured notes due 2028 are trading around 80 and have also declined due to the same reasons. Cerba has more than twenty-fours months to demonstrate improvements in key credit KPIs which could lead to twenty points of upside (principal plus two years coupon) in the case of the 2028 notes and forty points of upside in case of the 2029 notes.

Downside:- We feel the downside for the 2029 notes is material if operating leverage and deleveraging does not improve materially. The company would look to its shareholders for an equity injection to support a refinancing on terms which would favour the senior secured creditors. The downside for the 2028 notes is about ten points.

-

Unsecureds: There is limited ability for the unsecured to tighten, as secured debt currently prices at 5%. However, with underlying operational improvement likely to continue, there is only limited downside at mid 7%.

Hybrids: Depending on timing of any strategic asset sale and/or equity raise, the hybrids could have a further 5-10pts of upside. However, fundamentally they probably trade a little tight relative to the unsecureds and we could imagine some 5-10pts of correction to current levels instead. As an equity-like instrument, they are highly leveraged to the underlying rates environment, with a return to a low rate environment promising to be very beneficial to the Hybrids, but possibly too late to maintain the all-important rating.

-

Intrum: The book covers the bonds to approx. 50c/€ and at 4.5x EBITDA the Servicing business is worth another 25 cents (at 7x the bonds are par). So in case of a holistic restructuring, the bonds should trade to recovery value of 75c/€ - approx. where they are now. If the maturity structure is upheld, then the front end will layer the long end and the curve should be steep.

There is a risk of layering the bonds through a new AssetCo structure. We assume all bondholders will be invited to participate so as to generate the maximum coersion in a deal. But to benefit from this deal and risk manage the exposure, bondholders need to be able to roll into such new structures (qualified receivables).

-

INTU Debenture and SGS PIK Bonds have an equity return profile on their respective shopping centre asset pools. Upside comes from footfall and occupancy - each again close to pre-covid levels - and only when that has come back: higher rental agreements. Since the pandemic, the latter have been re-struck at low levels in an effort to re-build occupancy/footfall, sharply reducing overall net income at the individual shopping centres. However, with collection rates back above 90% and footfall and occupancy continuing to improve, the medium-term outlook has been improving.

However, the reducing consumer confidence and increasing interest rate environment is reducing theoretical valuations. There have been minimal large shopping centre transactions in the market and there is an underlying fear that several shopping centres, including SGS’s and Debentures’ need to change hands.

-

Lowell: In the low 70s, the bonds are value-covered by Lowell’s book, which lends significant downside protection. However, the company will have to restructure its balance sheet and over the next 12 months, there will likely be a series of catalysts that should put further pressure on the paper.

On the upside, we see little value above the book due to the small size of the 3PC business. Upside to the bonds or the business as a whole would therefore have to come from rate cuts. Those look likely to come but are probably better played in a name with less fur.

-

Matalan: The Super Sr. Notes and Priority Notes are risk-free. Should another restructuring be required - very much against our expectations - then first, the 2nd lien bonds could be layered by £40m and second, the se bonds would be the fulcrum - again.

The shares exhibit a typical risk profile for shares, although they appear deeply undervalued by our metrics.

-

Oriflame: Even as the top line seems to be bottoming out this year, Oriflame will have to restructure. Documentation is weak but foresees a Distressed Sale, which should become relevant in H224. The company has no debt-carrying capacity and would benefit from fresh cash. The unlikely upside case is that the Jochnicks hand over the keys - with the Russian business included. More likely is that the Russian business will be sold - possibly to someone close to the shareholder - to fund the last coupon payment in May 2024. In that case, we see value of around 20-30 cents. The downside is a fight over control and further asset sales.

-

Upside: Twenty-five points of upside plus twelve months of coupon payments. Pfleiderer, largely dependent on kitchen counters (somewhat oversimplified) is a macro play on the recovery in German real estate. The company has 12 months to show it is turning around sufficiently to try and refinance its bonds at par. We estimate the trough to be in H124 and improvements from there.

Downside: If the recovery in the financial results of Pfleiderer are delayed due to a weaker-than-expected macro environment or if the shareholder initiates a hostile action during the refinancing discussions within the next twelve months, the downside to the notes is approximately 30 which we have calculated at 5x trough EBITDA of EUR 80 million and deducting approximately EUR 200 million of drawn super senior & potential debt from baskets and dividing it by the bonds outstanding.

-

SBB needs its banks to roll their debt or liquidity from asset sales will mainly be used to de-risk back further whilst SBB will be unable to redeem even the front end of its bond curve. Nominally SBB has the cash to fund itself through to the end of 2025, but even that will require some cooperation from the banks.

We see the upside/downside of the August 27s as evenly balanced 18c/€ either side. Shorter-dated maturities have more downside, longer longer-dated maturities have less chance of ordinary redemption.

Conservative 50% LTV (on Sarria's valuation of assets - which lies 29% below the company’s) would create the bonds on average at 67c/€ today. But the longer banks roll and “buy out” the short-dated bonds, the further that value drops for those bonds remaining in the structure on the day that a process may need to manage the liabilities.

The continued failure to come to an agreement with the banks increases the possibility of a court process which would push the bonds lower. We would expect the company to be very vocal if they had come to an agreement with the banks. The next catalyst to review will be 9th November when the Q3 results are published.

-

Standard Profil: Bonds trading in the low 80’s giving 15% YTM (May ’26). The upside is limited in the short term as we await an uptick in overall OEM production numbers. Company benefits from recent order wins and should trade to 10% yield (7pts upside) if OEM production numbers start to improve.

Downside is limited as there are no meaningful upcoming maturities and there is limited debt ahead of the bonds. Liquidity remains an ongoing concern for us but at 15% YTM and recent support from OEMs, we see limited downside.

-

Tele Columbus : TC is headed for a restructuring, so the bonds are trading to recovery. Creditor position is relatively weak, which is why we pin the upside from an amend-and-extend at 80c/€ or 15 cents from current trading levels around 65c/€.

On the downside, we could well imagine the shareholders driving a hard bargain and shocking creditors into accepting a lower valuation before negotiations begin. We pin the fundamental value of the assets around 50c/€, perhaps worth 65c/€ in a generous auction on a good day. But if no deal can be reached, bonds should drop far lower.

-

Risk and return materially differ for any of the bonds depending on break-up or not of the WBS. In a no-break-up scenario, there is limited up- or downside as any movements will be primarily yield-driven as the A’s for instance already only trade less than two points wide of govies. The bond curve should largely maintain its shape. If, however, the WBS is broken up, then the long-dated As could earn up to forty points on the upside if their reinstated package includes equity. The downside would be equally unpredictable as likely a function of future water bills and new money requirement, which needs to be finalised by the company / Ofwat / creditors and which need to attract a willing investor.

-

Tullow: Strange scenario that the Senior Secured (15%) trade wide to the unsecured (12%) on the back of the recent new facility from Glencore to take the subs out.

Upside for the Unsecured is an early takeout, although participation in the previous tender was underwhelming. Par in March 2025 is the most likely outcome. Downside centres on oil price collapse and/or production issues.

The Senior Secured are more exposed to operational issues, given their May 2026 maturity, albeit the Company has deleveraged by operational cashflow and by sub-par tenders. 15% is attractive yield for Senior Secured Notes, and we see 7-8pts of upside for this bond to trade to 10%.

Similar downside risks as for the Unsecured, with additional exposure to the outcome of tax arbitration cases in Ghana. The Senior Secured Bonds do have some protection given their senior status, but the revolver will likely be drawn further and dilute recoveries. Mostly in the hands of original holders, the bonds should drop substantially into such a scenario before they recover.

NAMES UNDER CONSIDERATION

Auchan, Canary Wharf, Isabel Marant, Just Eat, Pizza Express, Very Group, Victoria Carpets

SARRIA News Flow